ThreeSixty Research Market Update - July 2012

JUNE MARKET PERFORMANCE (table)

Global economies

Global economies

Positive developments coming out of Europe throughout June helped boost markets and confidence across the globe.

However, the US and Chinese economies are showing signs of weakening which will likely remain top of mind for many.

US Economy

Starting with the world’s largest economy, a weakening in economic data over the course of June had the Federal Reserve (Fed) downgrade its Gross Domestic Product (GDP) growth forecast for the year to a range of 1.4%-2.4%.

As a result, the Fed has adjusted its expected unemployment rate for the year to be between 8% and 8.2%.

Lower consumption and consumer confidence data in May, combined with softer payrolls growth and general concerns about the world economy as a whole, were the catalysts for the downgrade.

This fuelled expectations that the Fed will introduce another round of quantitative easing (QE).

However, the impending ‘fiscal cliff’ has also been a much talked about topic in the US. The ‘fiscal cliff’ refers to a number of tax increases and spending cuts that are scheduled to take effect in the US in the coming calendar year.

If planned spending cuts and tax increases are implemented, a dampening of economic activity is likely, though the actual impact on the economy is still unclear.

In particular, the lead-up to presidential elections later in the year is likely to cause a delay in the implementation of some of the measures which could reduce their impact on the economy for 2013.

On a positive note, housing reports showed evidence that housing activity continues to recover in the US, with new home sales rising to their highest level in two years.

Europe

Moving to Europe, the pro-austerity New Democracy party won the Greek elections and European Union (EU) leaders agreed on a number of actions to support the troubled European economy.

The victory of the New Democracy party in the elections means Greece will stay on the austerity course and remain in the Euro.

However, the good news coming out of Greece was shadowed by worries over the state of Spain’s government finances and banks. It is estimated that € 62 billion is required to support the banks.

But it was the EU leader summit held in the last week of June that provided the kicker for markets.

Key announcements from the summit included the formation of a single bank supervisory mechanism, a € 120 billion growth pact and a “commitment to do what is necessary to ensure the financial stability of the euro area”.

It was agreed that the European Stability Mechanism will be able to assist banks directly rather than through governments.

The agreed € 120 billion growth pact will include infrastructure financing, tax policy pledges and support for small and medium sized businesses.

Markets had been expecting another round of talks with little action from the summit and subsequently rallied following the announcement of the outcomes.

The implementation of the actions is planned for July, however criticisms from Finland and the Netherlands are cause for concern, and it remains to be seen what shape the actual implementation of the agreements will take.

Australia

In news closer to home, minutes of the Reserve Bank of Australia’s (RBA) June meeting revealed that the decision to cut the cash rate was based solely on the current situation in Europe, and the concern that uncertainty will affect economic activity in Australia.

The Board is seemingly comfortable with the progression of the Australian economy and inflation is currently not the main driver in the cash rate decision.

It was therefore no surprise that the RBA did not further cut the cash rate in July.

In addition to the June rate cut, budget stimulus is reaching households across Australia in May and June.

Measures such as the School Kids Bonus and the Clean Energy Advance (to reduce the impact of carbon tax on families) took effect in May, and are expected to have a positive impact on retail sales in June and July.

Lower to middle-income earners in particular are expected to spend a significant proportion of these payments, with improvement in sales already being reported by retailers in some areas.

On the housing front, the RP Data-Rismark house price report for June was surprisingly positive with house prices rising 1% on average.

The increase in house prices comes after a very disappointing fall of 5.3% in May, which means the result for the quarter is now a slightly less disappointing fall of 1.2%.

In more positive news for Australia, after recent signs of weakness in the Chinese economy, China announced its first interest rate cut since the Global Financial Crisis.

Big movers this month

Going up – Financials +4.8%

Going down – Energy -6.2%

Equity markets

Markets this month performed well and regained some of the recent negative returns experienced in May. Large cap European listed companies provided investors with the highest returns of the majors.

Australian equities

Australian markets, as measured by the S&P/ASX All Ordinaries Index, were flat in June posting a small increase of 0.04%. Over the past year Australian shares remain well into negative territory.

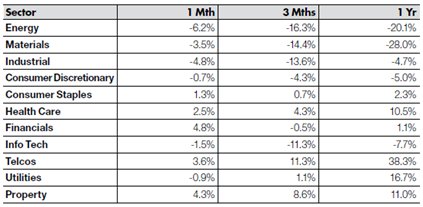

The sectors providing investors with significant headwinds again this month were Energy and Materials, with Industrials also having a tough month. Financials on the other hand was the best returning sector in June after being one of the worst performers the month before. Defensive sectors such as Consumer Staples, Health Care and Telcos once again performed well.

Over the 12 months to 30 June, Energy and Materials maintain their position as the poorest performers, while Telcos remain the best performing sector.

Global equities

Like most major indices, the Dow Jones Industrial Average had a positive performance of 3.9% over the course of June.

The Dow Jones Industrial Average 12 month return had been pushed into negative territory in May, when all major indices performed poorly. However, with the positive performance in June, the Dow Jones was the only major index seeing its 12 month return bounce back into positive territory.

It was good to see European indices among the positive performers this month, with the UK FTSE gaining close to 5%, and the Euro 100 increasing by more than 5%. In line with the Euro 100 gains, both the German DAX and the French CAC40 posted positive returns of 2.4% and 8.3% respectively. However, they are both still among the worst performers over the past 12 months.

In Asia, both Japan’s Nikkei and Hong Kong’s Hang Seng achieved positive returns for the month. The Nikkei was among the best performers of the major indices gaining 5.4%, while the Hang Seng also increased by more than 4%. Still the Hang Seng remains one of the worst performers over the past 12 months with a negative return of 13.2%.

Australian listed property this month outperformed global property. The S&P/ASX 300 A-REIT Accumulation Index increased 4.3%, while the UBS Global Investors Index, measuring performance of global property, returned only 0.3% over the month.

In the past 12 months Australian listed property has outperformed global property, however is underperforming over longer timeframes.

Fixed interest

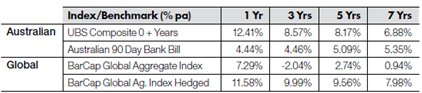

Australian bonds this month had a less favourable performance with the UBS Composite Bond All Maturities Index falling slightly by 0.16%.

The movement of the Australian dollar this month worked against unhedged global bonds, measured by the Barclays Global Aggregate Index which posted a return of -4.9%. Hedged global bonds on the other hand managed to escape the red, with a small gain of 0.14%.

Over the past 12 months Australian bonds have outperformed global bonds with hedged global bonds providing a return of 11.6% while Australian bonds have returned 12.4%

Australian dollar (AUD)

In June the Australian Dollar (AUD) recovered from the large drop it had experienced in May gaining 5.31% against the US Dollar (USD)

After occasional set-backs in June the AUD managed to move past parity with the USD once again at the end of the month.

The increase in AUD was in part a result of the RBA’s positive outlook on the Australian economy and the expectation of no further interest rate cuts for July. Healthy GDP and labour market data in Australia as well as positive news from Europe also helped the AUD.

The information contained in this Market Update is current as at 14/07/2012 and is prepared by GWM Adviser Services Limited ABN 96 002 071749 trading as ThreeSixty, registered office 150-153 Miller Street North Sydney NSW 2060. This company is a member of the National group of companies.

Any advice in this Market Update has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on any advice, consider whether it is appropriate to your objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance.

Before acquiring a financial product, you should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product.