What‘s ahead for Australian property?

The future of the Australian housing market has been the subject of much debate lately. Is it overvalued and if so, are we  likely to experience the same house price deflation seen recently in the US?

likely to experience the same house price deflation seen recently in the US?

An overvalued market?

Looking at historical and international comparisons, the Australian residential property market does appear to be fundamentally overvalued at the moment.

There are a number of valuation measures that point to this: the house price to rent ratio, the house price to income ratio, the magnitude of real and nominal house price appreciation and, the land to house price ratio.

But it’s housing affordability, the capacity of households to service their mortgages, that represents the greatest concern.

Rising debt

Housing affordability is likely the most significant factor affecting the housing market. The dramatic increase in mortgage debt has seen housing affordability deteriorate to a point comparable with the poorest levels of the past 20 years. This is despite a decline in interest rates since the late 80s and steadily rising household incomes.

In the absence of lower mortgage interest rates or higher household incomes, housing prices would need to decline to restore affordability to more sustainable levels.

What next for Aussie housing?

If the Australian housing market is fundamentally overvalued, does this mean local house prices are destined to experience the same savage price corrections we’ve witnessed in the US, Ireland, Spain, Japan and, Greece?

A moderate decline of around 10-15% in prices on average is certainly quite possible in the current environment. However, there may be special factors at work to prevent a more catastrophic collapse.

These special factors include the net shortage of available housing, particularly in capital cities,

However, there’s a tendency to view these special factors as supporting the case for house price appreciation no matter what. This may be a risky view,, particularly when these factors are at odds with powerful drivers like affordability.

Given the poor state of affordability, at best these special factors may reduce the magnitude of any potential decline in house prices rather than avoiding it altogether.

The outlook for mortgage interest rates is key to the outlook for Australian house prices. Current levels of mortgage rates are causing distress. If the Reserve Bank of Australia were to raise interest rates by another 25 to 50 basis points, then mortgage distress would likely escalate among the more exposed households. This would undermine house prices for the next year or two.

The long term view

There’s a widely held belief the Australian housing market always appreciates in the long term.

Because we haven’t seen significant price deflation or even stagnation across the entire housing market since the early to mid 1990’s, our memories of more difficult housing markets have faded with time.

There are also a large number of home owners who have either not lived through, or are too young to recall, anything other than rising housing prices.

However, looking back over the past 60 years periods of price deflation and stagnation have been as much a part of the longer term Australian housing story as has been price inflation.

Given the over-valuation evident in the housing market today and the existing poor levels of affordability, Australian house prices are unlikely to experience continued strong appreciation over the next few years. It’s quite possible we’ll see a period of anaemic house price performance, lasting five years or more.

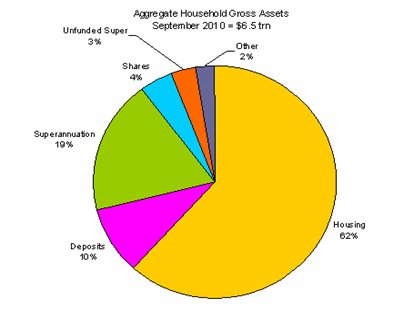

Unbalanced equity

A large portion of household wealth has been devoted to housing at the expense of other balanced diversification.

In fact, even though superannuation has become an increasing focus, housing remains the largest store of household wealth by a comfortably wide margin. This picture hasn’t changed much in the past 20 years.

The Australians bias towards housing is likely based on commonly held beliefs, namely

- the favorable tax treatment of housing compared with other investments

- the long period of perceived superior returns from housing, and

- the perception of housing is a low risk investment.

While the tax treatment for owner occupied housing in Australia is unquestionably favorable, its lack of a yield undermines its value as an investment. It’s purely a capital gains story and requires house prices to continue rising.

Investment property has a similar tax treatment to many other investments but offers the advantage of a rental income. However, the net rental yield, after allowing for a range of costs associated with managing and maintaining an investment residential property, is often significantly less attractive than that available from a range of other investments.

Despite having delivered strong returns over the past 20 years it’s expected returns from Australian housing are likely to be much less attractive on average looking forward. Other, less over-valued investments, are more likely to deliver superior returns over the next five years or longer.

Given this more cautious view of housing returns, the current high level of Australian wealth tied up in housing (around 62% at present) seems too high.

A greater diversification of Australian household wealth is likely to be beneficial as individuals look to securely fund their lifestyles ahead and in retirement.

Talk to your financial planner if you’d like more information on the role property plays in your portfolio.

Source RBA